FACTORING RESOURCES

Factoring 101

Feb 11, 2026

Many growing businesses face the same challenge: sales are strong, customers are reliable, but cash flow feels tight. When payments take 30, 60, or even 90 days to arrive, covering payroll, inventory, and operating expenses can become stressful.

Invoice factoring is one option businesses use to bridge that gap. This guide explains how it works, what it costs, how it compares to bank financing, and when it makes sense.

What Is Invoice Factoring?

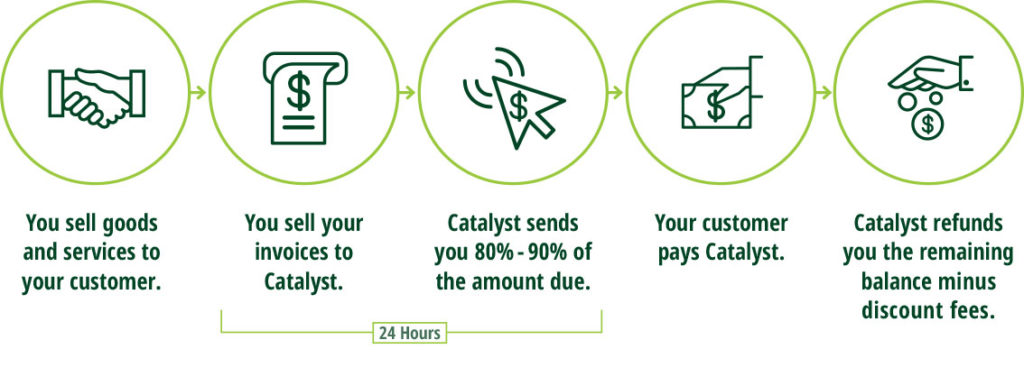

Invoice factoring—also called accounts receivable financing—is a form of working capital funding where a business sells its unpaid invoices to a factoring company at a discount.

Instead of waiting weeks or months to be paid by customers, the business receives most of the invoice value upfront. The factoring company then collects payment from the customer and releases the remaining balance (minus fees).

In simple terms, factoring turns invoices into immediate cash.

Invoice Factoring vs. Traditional Bank Loans

Many businesses are surprised to learn that they qualify for invoice factoring even when they don’t qualify for a traditional bank loan. This is because banks and factoring companies are evaluating different criteria.

| Feature | Invoice Factoring | Bank Loan / Line of Credit |

|---|---|---|

| Approval basis | Customer credit | Business credit & financials |

| Time in business | Flexible | Usually 2+ years |

| Speed | Days | Weeks or months |

| Debt on balance sheet | No | Yes |

| Collateral | Invoices | Often required |

| Use of funds | Flexible | May be restricted |

Key Differences

Factoring is not a loan.

You are selling an asset (your invoices), not borrowing money.

Approval focuses on your customers.

Banks evaluate your company’s credit, profitability, and balance sheet. Factoring focuses more on your customers’ ability to pay.

Factoring scales with growth.

As your sales increase, available funding usually increases as well.

Common Industries That Use Factoring

Invoice factoring is most common in industries where businesses invoice after delivery and wait for payment.

Typical industries include:

- Transportation and trucking

- Staffing and payroll services

- Manufacturing

- Wholesale distribution

- Oilfield services

- Construction subcontractors

- Logistics and freight brokerage

- Government contractors

These industries often operate with tight margins and long payment cycles, making steady cash flow essential.

Who Is a Good Candidate for Factoring?

Factoring is often a good fit for businesses that:

- Are newer and lack long credit history

- Are growing faster than bank limits allow

- Have customer concentration

- Are recovering from financial challenges

- Have strong customers but slow payments

It can also be useful as a temporary solution during growth phases, seasonal peaks, or transitions.

MORE ARTICLES

")